What affects your Credit Score?

Credit Education & General Information

A credit score is a numerical representation used by lenders to assess credit risk. Credit scores generally range from 300 to 850, with higher scores indicating lower perceived risk.

Credit scores are used in decisions related to mortgages, auto loans, credit cards, and other forms of credit. Lower scores may result in higher interest rates or limited approval options, while higher scores may help consumers qualify for more favorable terms.

What Affects a Credit Score?

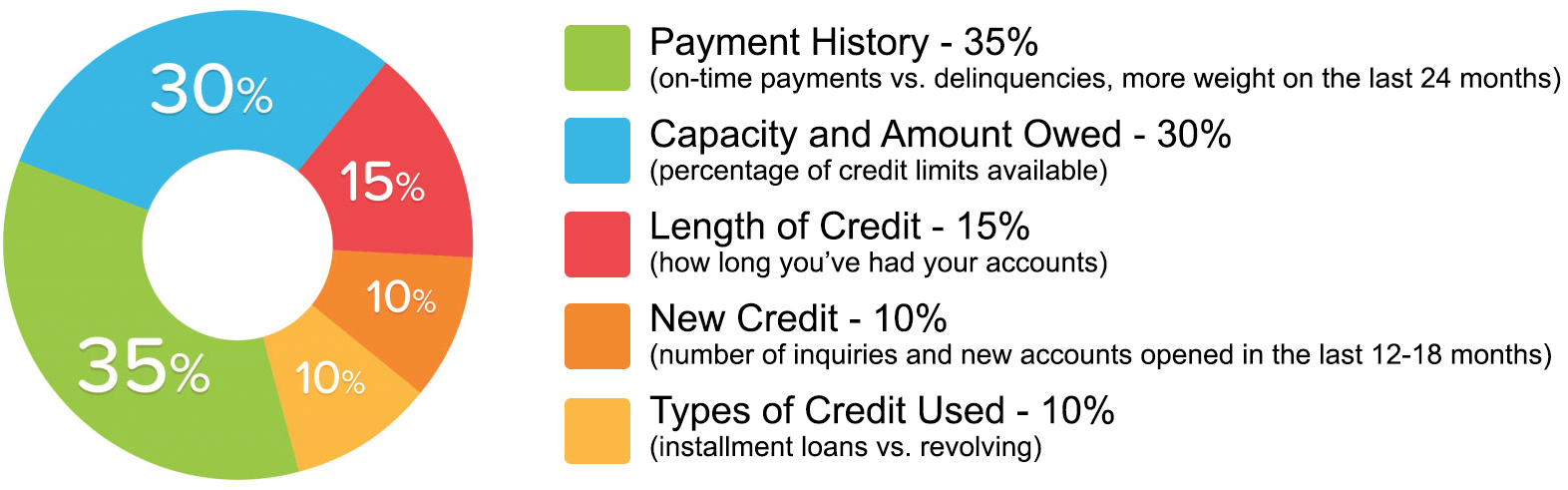

Credit scores are influenced by multiple factors, including but not limited to:

Credit Education & Responsible Credit Use

In addition to reviewing credit reports for potential inaccuracies, consumers may benefit from understanding responsible credit habits, including:

Credit Reporting Timeframes (General Information)

The following are general reporting timeframes under federal guidelines. Individual circumstances may vary.

Information That Generally Should Not Appear on Credit Reports

Under federal law, certain information is restricted from appearing on consumer credit reports, including:

Important Notice

This page is provided for general educational purposes only.

Savvy Smart Credit Repair does not promise or guarantee specific outcomes, removals, or credit score increases. Credit reporting decisions are controlled by credit reporting agencies and furnishers.

A credit score is a numerical representation used by lenders to assess credit risk. Credit scores generally range from 300 to 850, with higher scores indicating lower perceived risk.

Credit scores are used in decisions related to mortgages, auto loans, credit cards, and other forms of credit. Lower scores may result in higher interest rates or limited approval options, while higher scores may help consumers qualify for more favorable terms.

What Affects a Credit Score?

Credit scores are influenced by multiple factors, including but not limited to:

- Payment history

- Credit utilization (debt-to-available credit ratio)

- Length of credit history

- Credit mix

- New credit activity

Credit Education & Responsible Credit Use

In addition to reviewing credit reports for potential inaccuracies, consumers may benefit from understanding responsible credit habits, including:

- Making payments on time

- Monitoring credit reports regularly

- Keeping credit card balances relatively low compared to available limits

- Using credit responsibly and consistently

- Maintaining older accounts when appropriate

Credit Reporting Timeframes (General Information)

The following are general reporting timeframes under federal guidelines. Individual circumstances may vary.

- Late payments: Up to 7 years

- Collections: Up to 7 years from original delinquency

- Charge-offs: Up to 7 years from original delinquency

- Closed accounts:

- Negative: up to 7 years

- Positive: up to 10 years

- Bankruptcy:

- Chapter 7: up to 10 years

- Chapter 13: up to 7 years

- Inquiries: Up to 2 years (most impact within first 12 months)

Information That Generally Should Not Appear on Credit Reports

Under federal law, certain information is restricted from appearing on consumer credit reports, including:

- Medical details without consumer consent

- Certain outdated negative information

- Personal demographic details unrelated to creditworthiness

Important Notice

This page is provided for general educational purposes only.

Savvy Smart Credit Repair does not promise or guarantee specific outcomes, removals, or credit score increases. Credit reporting decisions are controlled by credit reporting agencies and furnishers.

Educational content only. Results vary.